May 19, 2026

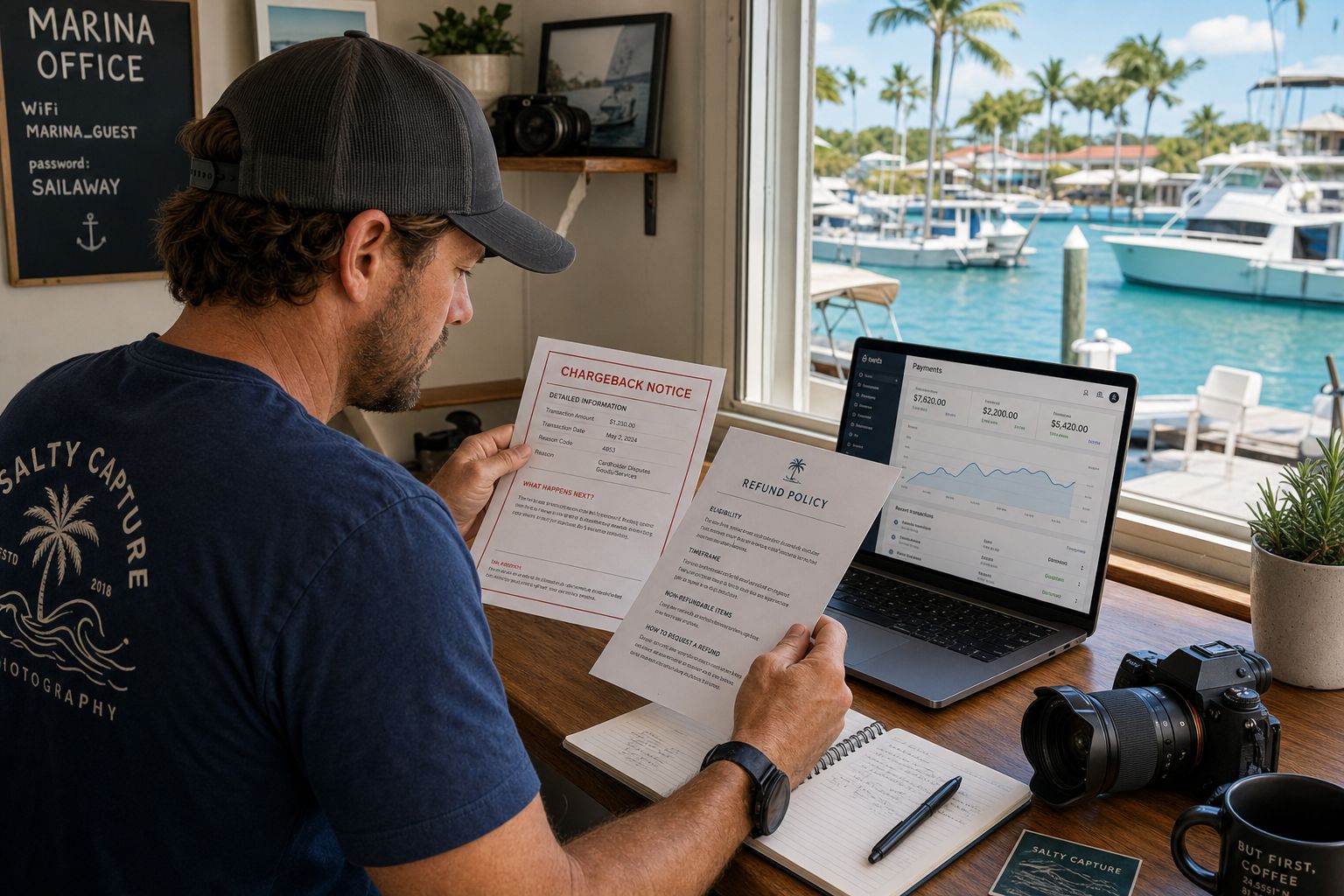

I had a captain call me from Simpson Bay once, completely rattled. He had run a private sunset charter the week before - nice group, big boat, no complaints, guests left happy. Then he woke up to a dispute notification. The guest had gone to their bank and claimed the charge was unauthorized. He had nothing. No signed waiver, no check-in sheet, no photo of the group on board. Just a booking confirmation he had sent from his personal Gmail.

He lost the dispute in three days. Lost the money, paid the dispute fee, and had to eat it.

This is what chargebacks actually look like for Caribbean tour operators. Not some rare fraud edge case. A real guest who either forgot what they booked or decided to try their luck, and an operator who had nothing to show a bank reviewer who has never visited St. Maarten and has sixty seconds to make a call.

When you accept a card online, you are selling a future experience to someone you have never met. That is exactly the scenario banks are designed to be suspicious about. Card-not-present, service delivered later, guest on a phone somewhere in a different country.

Your job is not just to collect money. Your job is to make every payment look obviously legitimate to three audiences: your guest, their bank, and your payment processor.

3D Secure - branded as Visa Secure or Mastercard Identity Check - adds an authentication step for certain online card transactions. When it triggers, liability for fraud disputes shifts away from you and onto the cardholder's bank. That is the part you care about.

But here is what a lot of operators miss: 3D Secure only helps with "I did not authorize this" fraud disputes. If a guest claims "service not provided" or "refund not processed", you still need documentation. Authentication is not a substitute for a paper trail.

For private charters and high-ticket trips, taking full payment months ahead makes guests nervous. That anxiety is a chargeback risk by itself. A deposit structure reduces it, but only if the timing makes sense.

When you fight a dispute, you are not arguing with your guest. You are sending a document package to a bank reviewer who has never been to your island and has about sixty seconds to decide if you look credible.

Short, specific, and consistent. One screen on a phone. Exact deadlines, not vague language like "reasonable notice." Same rules on your website, in the confirmation email, and on any OTA listings. If your policy says 24 hours on your site and 48 hours in the email, you have already lost.

Two moves that cut disputes fast:

The captain I mentioned at the start lost because he had nothing to show. You do not need a lawyer to win a dispute. You need a folder.

Build this as a crew habit: after every trip, someone uploads the check-in sheet and signed waiver to the booking record. That one routine can save you thousands over a season. I have watched operators lose dispute after dispute not because they did anything wrong, but because they could not produce a clean story in the format a bank needs. You can do everything right and still lose if you cannot show it on paper.

That captain would have won with a single timestamped photo of the guests on board and a check-in list. That is it. Everything else - the 3D Secure setup, the deposit timing, the policy language - those are layers on top. The foundation is just: did you do the trip, and can you prove it?

Run a checkout that shows guests exactly what they bought, send the confirmation immediately, and document the day of every trip without exception. We built Junglebee to handle the checkout, the deposits, and the booking records automatically - but honestly, start with the photo habit. It costs nothing and it works every time.